What is a 1031 Exchange?

When I first started in real estate in 2003, I worked as a 1031 exchange buyer's agent specializing in "Credit Tenant, Bond, and Net Leased Investments in the Western Five." I had no idea what it meant at the time, but it sounded sophisticated, paid a small salary, and it got me to places like Colorado Springs, Bakersfield, and Gilbert.

I felt like I had learned a secret working there; a 1031 exchange isn't a tax loophole. It's a capital strategy that separates investors who think long-term from those who cash out and wonder where the money went.

A 1031 exchange, named after Section 1031 of the Internal Revenue Code, is fundamentally simple: you sell one business, property, or investment asset and swap it for another without triggering immediate capital gains tax. On paper, it sounds straightforward. In practice, it's a legal minefield where one missed deadline or one vesting misalignment costs you everything the tax code promised to defer.

The Four Necessities: What Actually Matters

1. Property Qualifications: "Like-Kind" means real estate for real estate

Properties involved in a 1031 exchange must be held for productive use in trade or business or for investment, and they must be classified as “like kind”.

“Like-kind" for real property means any real property held for investment or business use can be exchanged for any other real property held for the same purpose. A commercial office building can exchange for agricultural land. An apartment complex can become a shopping center. The IRS doesn't care about use similarity anymore—just that both properties are real property held for investment or business.

2. Timeline:

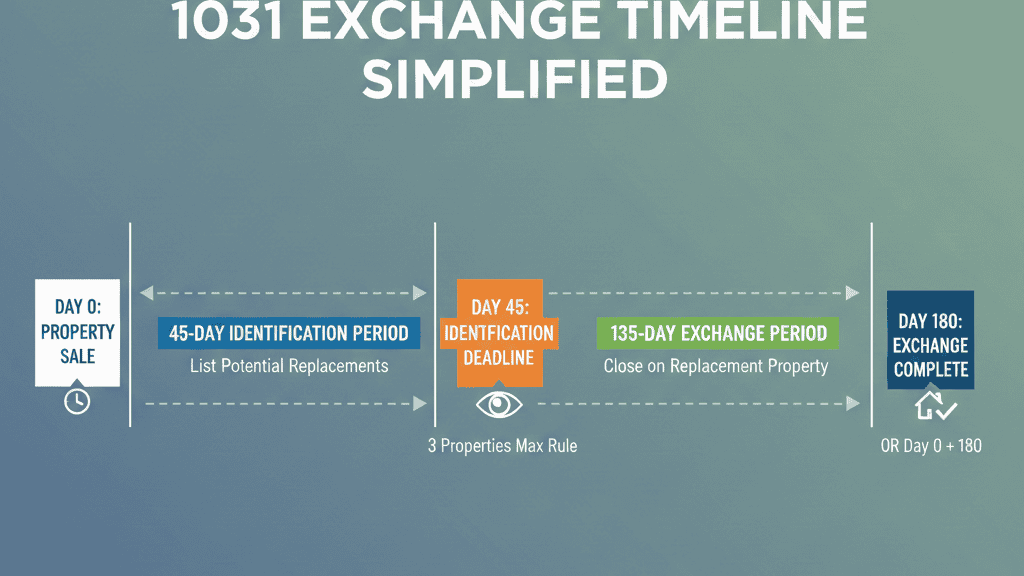

The IRS provides a maximum of 180 days to complete an exchange, measured from the close of escrow (COE) on your relinquished property. Not 181 days. Not "close enough." Midnight on the 180th day is your deadline, and the IRS enforces it with zero discretion.

But before you close on your replacement property, you have to identify what you're buying. And that deadline comes first.

The 45-Day Identification Requirement

By midnight on the 45th day of the exchange, you must identify all potential replacement properties in writing. The description must be unambiguous—vague references or "a property in Oakland" won't pass IRS scrutiny. You need legal descriptions, addresses, and enough detail that there's no confusion about what you're identifying.

Missing the 45-day deadline is the most common fatal error in 1031 exchanges. Your qualified intermediary—the third party required to hold the funds during the exchange—cannot accept replacement property identification after day 45, even if you close on day 30. The identification window closes. Period.

The 180-Day Completion Requirement

From COE of your relinquished property to COE of your replacement property (or properties), you have 180 days. If you identify replacement properties but don't close by day 180, the exchange fails, and your capital gains tax comes due immediately. This isn't negotiable with the IRS, and it's not something you can extend or work around.

Real-world impact: if you're selling in a slow market or your lender is dragging on underwriting, this timeline becomes a pressure point. Title companies know this. Lenders know this. Make sure your team understands it matters more than their convenience.

3. Identification

Once you enter an exchange, you have two options for identifying replacement properties. Choose carefully—the IRS doesn't let you switch strategies mid-exchange.

The 3 Property Rule

You can identify any three properties, of any price, anywhere in the United States. This is the simplest pathway. You're not limited by value, location, or timing—just the count. Three properties maximum.

This works well when you know exactly what you're replacing your property with, or when you have two or three strong prospects and want flexibility to choose based on which one closes fastest or offers the best terms.

The 200% Rule

If three properties aren't enough, you can identify four or more properties—but with a constraint. The combined fair market value of all identified properties cannot exceed 200% of the fair market value of the relinquished property.

Example: You sell a property valued at $1 million. Using the 200% Rule, you can identify replacement properties totaling up to $2 million in combined value. You're not required to buy all of them—you just can't identify more value than the rule allows.

The 95% Exception (Often Overlooked)

Here's where most people miss a critical nuance. If you identify more than three properties, and the aggregate value exceeds 200%, you can still proceed—but only if you actually acquire 95% of the total value you identified. This is the backdoor that lets you identify $5 million in properties against a $1 million sale, provided you close on at least $950,000 worth of identified properties.

Many exchanges fail because investors don't understand this exception exists, or they misuse it. Know it. Use it strategically.

4. Tax Deferral

Here's the promise of a 1031 exchange: defer 100% of your capital gains tax liability. Here's the catch: you have to follow the rules exactly.

To defer 100% of capital gains tax, two conditions must be met simultaneously:

Reinvest All Cash

Every dollar generated from the sale of your relinquished property must go into the replacement property or properties. If you pocket $100,000 in proceeds, that $100,000 becomes taxable income immediately. The qualified intermediary holding your funds is there to ensure you don't touch the money during the 180-day exchange window.

What this means: your loan proceeds from the sale, your equity, your down payment—everything must be deployed into replacement property. No exceptions, no partial deferrals.

Equal or Greater Value

The replacement property (or combined properties, if you're buying multiple assets) must equal or exceed the fair market value of the property you sold.

Sell a $1 million property? Buy replacement property worth at least $1 million. Sell for $1 million and buy for $900,000? You've triggered capital gains tax on the $100,000 shortfall. The IRS calls this "boot"—taxable proceeds that weren't reinvested.

The Boot Trap

Boot comes in multiple forms: cash you don't reinvest, debt relief (if your new property has less financing than your old one), or property received that doesn't qualify as like-kind. Each creates a taxable event. Sophisticated exchangers structure deals specifically to avoid boot, which is why this isn't a DIY process.

The Vesting Question: Why Your Name (or Entity) Matters

Here's a detail that trips up more exchanges than the timeline. The taxpayer who sells must be the same taxpayer who buys.

This usually means identical vesting—if John Doe's name is on title to the relinquished property, John Doe's name goes on the replacement property. But what if John wants to change how the replacement property is held?

The Real Lesson

A 1031 exchange isn't about being clever with the IRS. It's about understanding that capital preservation in real estate depends on structure, timing, and absolute adherence to the rules.

If you're considering a 1031 exchange, don't treat it as something you'll figure out with your tax guy after closing. Build the strategy before you list. Hire a qualified intermediary before you sell. Identify replacement properties before you're desperate. And if the timeline or the math doesn't work, walk away. Forcing an exchange that doesn't fit your circumstances is how you end up paying the capital gains tax you were trying to avoid—plus penalties.