You are trying to figure it out and by "it" I mean all of it—relationships, family, career, friends, clothes, food, being cute, and why you're still renting.

You make $186,600 a year—the current Area Median Income for San Francisco County. Solid job, decent credit, and money in the bank yet, you're still paying $4,000 a month for a place with no garage and pet rent.

Every month you watch your rent disappear into someone else's equity while you keep on wondering where all your money is going; how much was that chorizo burrito from the food truck? The truth is it is hard to believe you're ready when you feel broke all the time.

The feeling of being broke isn't a character flaw. It's math.

You're not actually broke—you're just spending every dollar the moment it lands. Rent takes the first $4,000. Food, insurance, phone, that one hobby that costs more than it should—it all adds up fast.

What's left feels like nothing, even though you make good money. The gap between your income and your actual cash on hand is real. It's frustrating. This is the reason why renters think they can't buy.

But you can. The path just requires seeing your money differently.

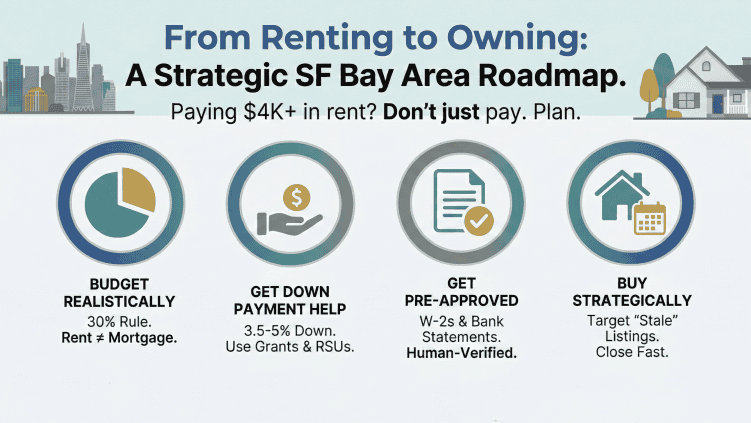

Step 1: Rent Into a Real Budget

If you're paying $4,000 a month in rent, you've already proven you can handle a $4,000 housing payment.

A realistic rule of thumb: keep total housing costs (principal, interest, taxes, insurance, HOA) under 30% of gross income. On $186,600, that's about $4,650 per month. Work backwards from that number with your lender, not from the listing price you saw on Zillow.

Here's where most renters trip up: they forget that rent and mortgage aren't the same animal. Rent doesn't include property tax (San Francisco hits you with 1.25% annually), insurance, or the thousand little repairs a landlord used to handle. Miss those numbers and you're not buying a home—you're buying stress.

This is where tech workers have a quiet advantage: equity and bonuses. If your RSUs, bonus, or refresh cycles are part of the down payment, make sure they accessible and not on your CAP sheet.

Step 2: Get a Little Help With Your Down Payment

The biggest hurdle to homeownership is the down payment and it doesn't have to be. You don’t need to bring in 20% down to buy a home; you can come in with as little as 3.5-5% and that doesn’t have to come from you.

Down payment assistance programs exist for this moment. California, San Francisco, and individual lenders all have programs that can reduce or eliminate the gap between what you've saved and what you need to close.

CalHFA (California Housing Finance Agency) offers loans that cover up to 20% of your purchase price with zero interest. They're designed for first-time homebuyers earning up to 140% of Area Median Income—you qualify comfortably.

San Francisco's First-Time Homebuyer Assistance Program goes further. Depending on your income and the property price, the city can fund up to 15% of your purchase price as a down payment grant—not a loan, a grant. You don't pay it back. The money comes from the city's housing trust fund, and they're actively trying to move it. Applications open year-round; most people don't know about it.

Research your options before you talk to a lender. Go to CalHFA.ca.gov. Call San Francisco's housing finance office or downpaymentresource.com. Ask your employer if they offer down payment assistance—tech companies increasingly do. Then bring that information to your pre-approval meeting and ask the lender which programs they can layer into your deal.

Step 2: Get a Real Pre-Approval

Fortune may favor the bold but real estate rewards the ordinary. Predictable. Boring. Conventional. A lender doesn't want to hear about your brilliant side hustle or your equity refresh that's coming next quarter. They want to see your W-2, your bank statements, and a credit score that doesn't make them nervous.

Banks want to lend money to people; they want to lend money to you; make sure to talk to a mortgage person and get a pre-approval letter. After you go quicken.com (I know…why deal with people?), go to your financial institution and get a pre-approval letter; real estate is intrinsically human.

Step 3: Interview a real estate agent

The NAR settlement in August 2024 changed how buyer's agents get paid. The seller no longer automatically posts your agent's fee in the MLS. Now you sign a written buyer-broker agreement before touring anything.

Three things are true in 2026:

First you must sign that agreement upfront and second it must spell out how your agent is paid. Three: the seller is no longer required to offer compensation.

In practice, sometimes the seller still pays your buyer's agent through an off-MLS offer. Sometimes you pay your agent directly, flat fee, hourly, or percentage. Sometimes you negotiate a seller credit that covers the fee at closing.

Step 4: Stay in Reality

Most renters start with "I want to stay in San Francisco." Fair. But you need to decide what you value: commute versus space, condo versus single-family, new construction versus older building in a walkable neighborhood.

A one-bedroom condo walkable to SoMa maximizes lifestyle but tanks your square footage per dollar. Cross the bridge to Oakland or Berkeley, and your down payment buys more space, often a small yard, and less stress. The trade-off is real.

Step 5: Offers to Purchase

In San Francisco Bay Area, new properties get multiple offers. You're competing with all-cash buyers, founders with secondary liquidity, and adult children backed by parental wires. You don't beat them on price or terms so it’s time to stay prepared and get strategic.

Opportunity lives after 20 days on market; fresh listings get a feeding frenzy of offers. Stale listings get a seller who's starting to wonder if the price was wrong. A property that's been sitting for three weeks means the market already told the seller something—maybe it needs work, maybe the neighborhood's not as hot as they thought, maybe they priced it wrong. Whatever the reason, that seller is more flexible than the one with five offers in their first week.

When you find one, move fast. Clean pre-approval from a respected lender, short timelines (14–21 day close instead of 30+), tight contingency periods. That's your competitive advantage. You're not outbidding the cash buyers; you're showing the seller you won't disappear into underwriting hell for 45 days.

Step 6: Plan Your Cash Beyond the Down Payment

One of the reasons I started selling real estate because I was too intimidated to ask a simple question, “How much is this going to cost…?”

If you don’t want to worry about doing laundry at your parents and bringing your lunch to work remember that there are closing costs (typically 2–3% of purchase price), you’ll need to pay and plan for them; the seller can cover some non-recurring closing costs (NRCCs), but your agent will need to ask.

For Now

The San Francisco market in 2026 isn't impossible. Renters who win aren't the ones with the highest salaries—they're the ones who know their real monthly number, get serious pre-approval, understand that there are additional costs involved, and make clean, believable offers.

Ready to stop renting? Let's figure out your actual number. Reach out—I'll walk you through it. You're already doing the hard part every month when you pay rent here. The rest is just learning new rules and using them on purpose.