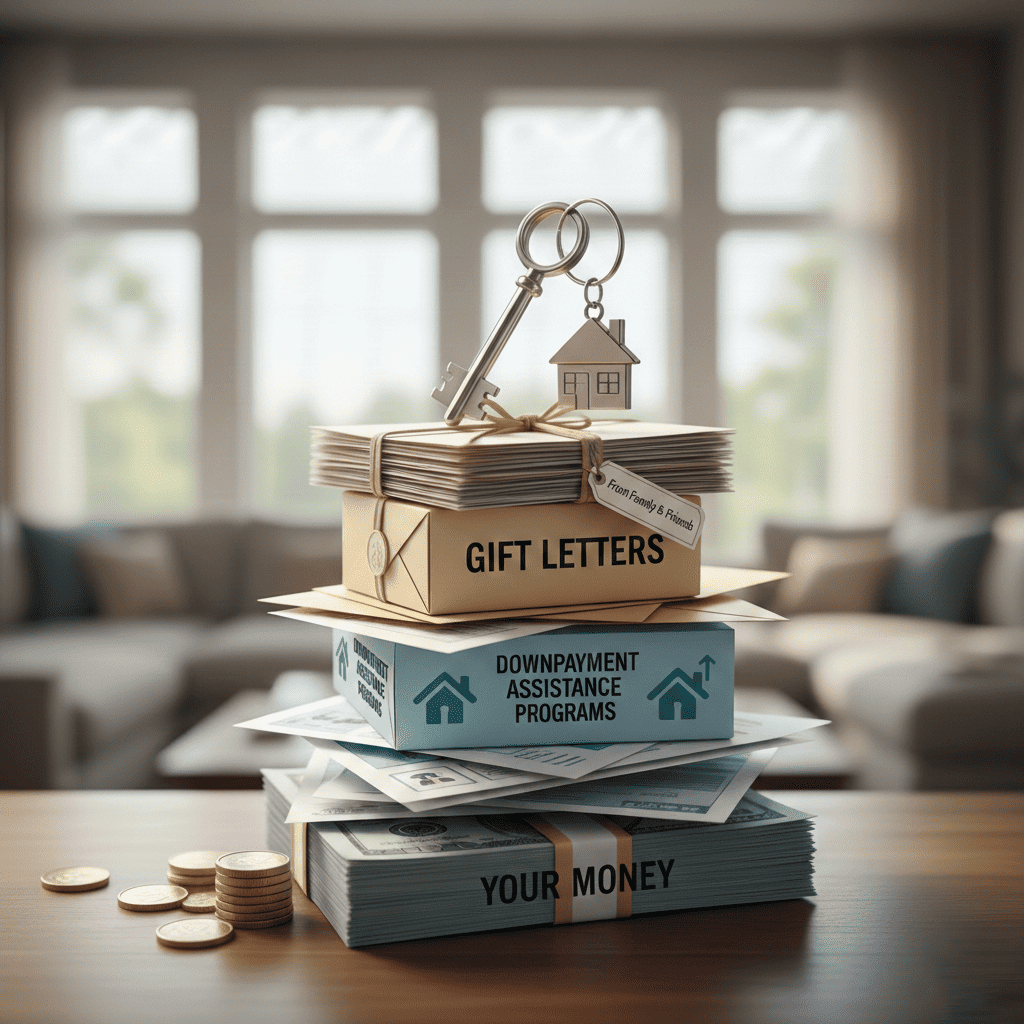

Stacking Gift Funds, Down Payment Resources, and Your Money to accelerate your process.

If you know what I’m talking about carry-on Miss Thing… for those who don’t know what I’m talking about:

In the old days, Maybelline (makeup) ran an iconic ad campaign with the tagline "Maybe she's born with it. Maybe it's Maybelline." The messaging was clear, some women looked naturally flawless; others achieved it through makeup.

When Poppa Grim saw a young person who owned a home, he'd sing the Maybelline jingle. Because he thought their parents helped him—which as we found out later in life was correct.

And We’re Back

Stay in the Bay Area, where your salary makes sense? A median home price hovers around $1.3 million.

Move back home to wherever—Des Moines, Boise, rural Vermont, the suburbs of your childhood—where a decent house costs $350,000? Your salary drops 30 to 40 percent. Suddenly you’re earning $50,000 to $60,000 annually. The math works differently, but the loss feels visceral. You traded earning potential for affordability. That’s not a win.

This is the conundrum that defines our generation’s relationship with homeownership. The money is amazing, but housing costs in the places where money exists are stratospheric.

You can’t afford to stay. You’re not willing to leave. So, you’re paralyzed. And we do not like paralyzed.

What to Do?

In my best Edina Monsoon (grrr, AbFab) voice, “It’s Stacking sweetie, look it up.”

Stacking is the strategy of combining multiple funding sources—your savings, gift money from family, down payment assistance grants, employer programs, and sometimes even forgivable loans—into a single down payment that makes homeownership possible without sacrificing either your income or your location entirely.

It’s knowing how the system works and using every available tool at once.

The Three Layers of Stacking

Foundation Your Money

This is the unsexy part. It requires discipline. But it’s also the foundation that makes everything else possible. Lenders want to see that you’ve contributed something. They’re not looking for massive amounts—they’re looking for evidence that you’re serious.

Start with what you control, what you’re spending. I had to get an accountability buddy to save money. I had a rule that if I already owned something, t-shirts and gym clothes and shoes for example, and I wanted a new one that costs more than $20 I would call a friend. It saved me a lot of money. But it adds up real capital that sits in your account, under your control, and proves to lenders that you can prioritize long-term goals over short-term wants.

Layer Two, Down Payment Assistance

Most people don’t know these programs exist and if they do know don’t think they can qualify, or assume the process is too complicated; they exist and most people can qualify.

Over 2,300 down payment assistance programs exist—federal grants, state initiatives, nonprofits—local funds designed for people earning what you earn, with credit like yours. Programs range from free grants to forgivable loans (forgiven if you stay 5–10 years) to below-market rate loans.

Start at DownPaymentResource.com. Answer basic questions about location, income, and situation. You will be matched with real programs you qualify for. Apply online (15–30 minutes per application), wait 2–4 weeks for approval, and coordinate funding with your lender at closing.

Layer Three Gift Money

Parental help matters, but it’s not the only option—and it doesn’t require shame or strings. A gift letter is simple: one page stating the money is a gift, not a loan, signed by both gift giver and giftee. Your lender verifies it with bank statements. That’s it.

The real power of gift money isn’t the amount. It’s a signal that someone believes in you enough to back your dream. That belief strengthens your mortgage application and can lower your interest rate by demonstrating access to capital beyond your salary.

If your parents can’t help, you’re not stuck. Plenty of buyers stack without parental gifts. But if they can—even $5,000 or $10,000—it matters more than you think.

The Stack:

- Your savings: $28,000

- Parental gift: $15,000

- Down payment assistance grant (from state program): $27,000

- Employer down payment assistance (many tech companies offer this): $5,000

- Total available: $75,000

What That Buys:

A $900,000 home typically requires 5 percent down ($45,000) plus closing costs (2 to 3 percent, roughly $18,000 to $35,000). Your stacked funding covers the entire down payment and most closing costs. You’re not borrowing more. You’re not stretching. You’re done.

Your lender coordinates everything. You provide the gift letter from your parents, bank statements proving the transfer, and DPA approval documents from the programs you qualified for. They verify. They approve. You close.

Timeline

It’s not instant. But it’s also not “years away.” If you start today, you could have keys before this time next year.

From decision to keys in hand, here’s what the process looks like:

Month One: Research lenders, identify your loan type, talk to parents about whether a gift is possible, visit DownPaymentResource.com and identify qualifying programs.

Month Two: Apply for down payment assistance programs. Start accumulating additional savings if possible. Get pre-approved with your lender (this is where they confirm your borrowing capacity and which gift/DPA sources they’ll accept).

Month Three+: Shop for homes, write offers, get your DPA programs approved, collect gift letter and documentation from family.

Month Four: Inspection, appraisal, final coordination with lender to confirm all funding sources are verified and ready for closing.

Month Five: Close on your home.

For Now

You don't need luck. You don't need a trust fund. You don't need to choose between earning potential and affordability. You need to know that 2,300 programs exist to help you, that your savings matter, that your family's belief in you has concrete financial value, and that a lender will coordinate it all into a down payment.

I have a full set of financial calculators on my website: americasells.com