Let me preface this by saying there will always be all cash $300k above asking price in two day offers to talk about, but those are now the exception and not the norm. Real estate is cyclical with each new market cycle bringing some fresh new hell for agents, buyers and sellers. And the fresh new hell for a lot of newer agents is the coming balanced market. The new “norm” is boilerplate and that means loans and contingencies are back.

To put some numbers to this shift Realtor.com projects that the national housing market will average about 4.6 months of supply in 2026, which they describe as “balanced territory,” with inventory up roughly 8.9% year‑over‑year. This move toward mid‑single‑digit months of supply and rising active listings is exactly what you’d expect as the market transitions away from an extreme seller’s market into more balanced condition

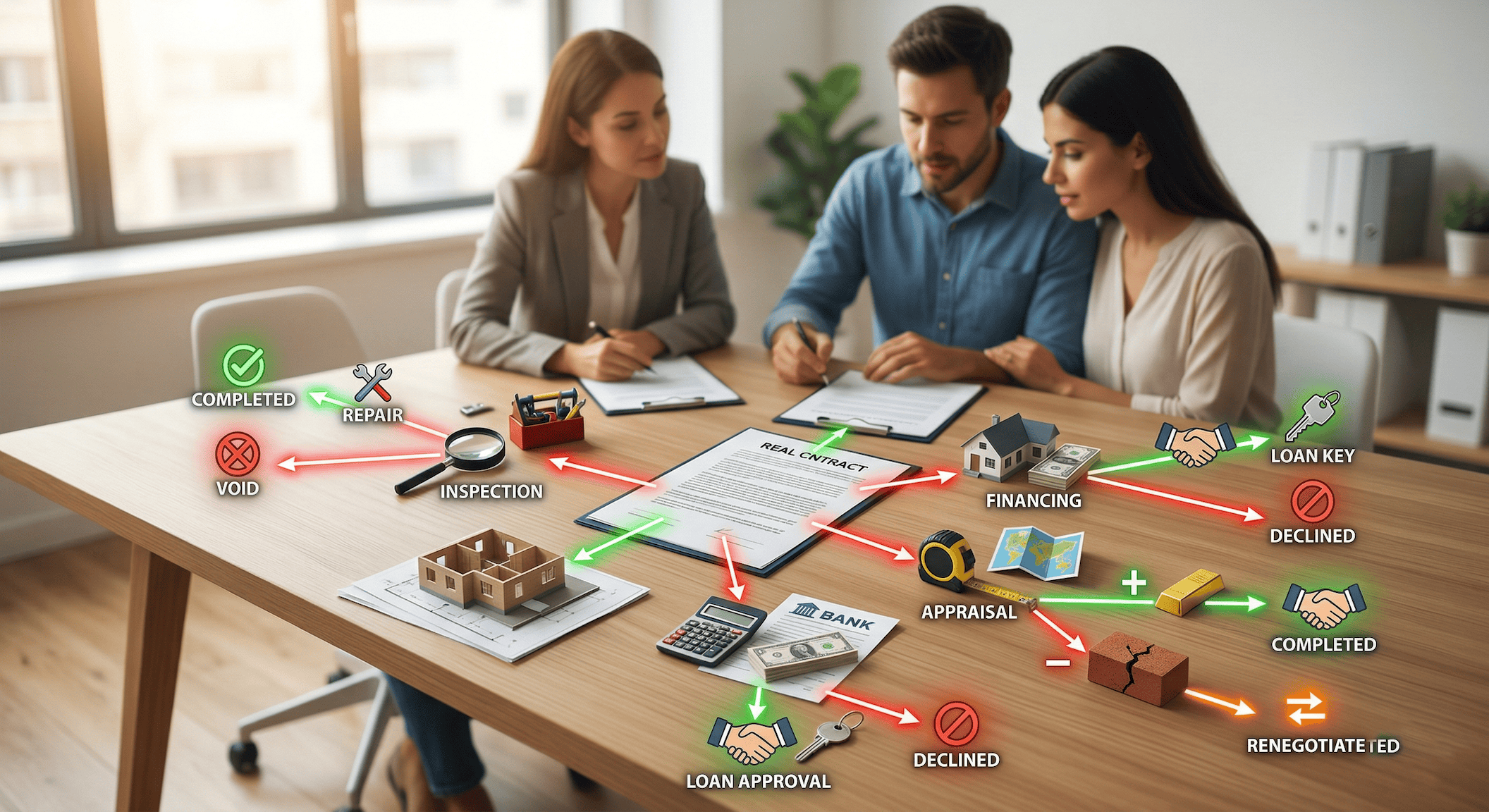

Contingencies

Most people think of contingencies as an escape hatch—a way to back out if things get weird. They can be, sometimes, but mostly they're a scheduling device with teeth. They create deadlines, force decisions, and keep the transaction from drifting into fantasy. In markets where rates move, insurance gets complicated, and the house that looked perfect on Sunday can reveal a cracked foundation by Wednesday, that structure is keeps deals happening and you (agents and clients) protected.

What Contingencies Actually Do

Contingencies protect both sides. They give buyers a limited window to verify what sellers disclosed, inspect the property, confirm financing, and make sure the deal is actually what they thought it was when they signed.

They give sellers protection too—they force buyers to move. Real estate markets are volatile. Sellers don't need a buyer camping on the property for three weeks while they decide whether they're emotionally ready to own a house. The contingency deadlines force action. Either the buyer investigates, removes contingencies, or walks. The seller doesn't wait indefinitely.

Earnest Money

That's where the earnest money deposit comes in. It sits in the middle of this entire structure. The deposit tells the seller the buyer is serious. The contingencies tell the buyer they have a protected window to do their homework. If the buyer cancels during a valid contingency period—and does it in writing and on time—the deposit gets returned. If the buyer waits too long, removes contingencies, and then tries to back out, the deposit becomes vulnerable.

The Contingencies That Matter Right Now

California's standard purchase agreement lists contingencies in a few key places, and most agents are still operating from memory instead of actually reading the current forms. That's a problem.

Loan Contingency. The buyer gets time to obtain the financing specified in the contract.

Appraisal Contingency. The property has to appraise at or above the agreed price. If it doesn't, the buyer has options—renegotiate, bring more cash, or walk.

Investigation of Property. This is the broad one, and it's doing most of the heavy lifting. This is the buyer's chance to inspect the physical condition and investigate anything else affecting the property—permits, zoning, neighborhood issues, environmental hazards, square footage, utilities.

When an agent says, "you've done your inspection," they usually mean "you had a general inspector out there." Those are not the same thing. A thorough investigation means hiring specialists when needed and actually reviewing what they find.

Insurance Contingency. This one got separated out in recent form updates for a reason. Insurance used to be something people assumed would sort itself out. That's no longer true in California. Carriers have stopped writing new business in parts of the state. Others impose physical condition standards before issuing or keeping a policy. Knob-and-tube wiring, old roofs, missing defensible space, and dated plumbing are no longer charming period details. They're underwriting red flags. A buyer can be fully qualified for the loan and still have a real problem if they can't get affordable coverage.

Review of Seller Documents and Title. The buyer gets to assess what's on paper, not just what looks pretty in person. Preliminary title report, disclosure documents, HOA records if applicable—these tell the story the property itself won't.

The Pressure Points

Leased or Liened Items. Solar panels are the obvious one, but not the only one. Water systems, propane tanks, and other ongoing obligations all fall here. If the seller discloses leased equipment, the buyer gets to review those terms and decide whether they're willing to assume them. This used to get buried in a stack of paper. It shouldn't. Read the terms. Understand the cost. Know what you're inheriting.

Insurance as a Standalone Issue. Seriously—your ability to get insurance is not part of the loan contingency. It's separate. That distinction matters. Start investigating insurance availability and cost early. Don't wait until five days before closing to discover you can't get coverage at any price.

Timelines

Here's what most people miss: contingency deadlines are not suggestions. They're the structure that keeps the transaction honest. The buyer has to inspect, review, and decide. If the buyer doesn't act within the deadline, the seller can issue a Notice to Perform. If the buyer still doesn't move, the seller can cancel the agreement.

The earnest money deposit proves the buyer is serious. The contingency calendar proves whether they actually are. In a market where one missed deadline can turn a protected deposit into a disputed one, that's not a technicality. Make sure to pay attention to your paperwork and create an escrow calendar.

The Bottom Line

Don't waive contingencies without understanding what you’re getting yourself into. Don't assume inspection means one general contractor walked through the house. Don't treat insurance as a side conversation. Contingencies exist to protect you—but only if you use them.