There is something to be said about practicing, whatever it is one does for work, and specialization; the constant exposure to terminology makes it less necessary to write explainers and pass them off as content… but here we are.

As you know or can guess, I write these explainers because I need a refresher myself. GRM is one of those outliers I learned early in my commercial real estate days back in 2003, and then promptly filed in the back of my brain behind "1031 exchange timelines", “N or NNN” and "which appraiser returns my calls." But recently I've had more clients ask about rental properties, and GRM keeps coming up. Time to pull it back out and dust it off; it’s an easy way to target properties.

The Gross Rent Multiplier is the fastest way to tell whether a rental property is worth a second look. It will not tell you if a deal is good. It will tell you if a deal is worth the effort of finding out if it is good. Use it along with CAP rates to quickly find some wheat in deals. (wheat from the chaff… c’mon people)

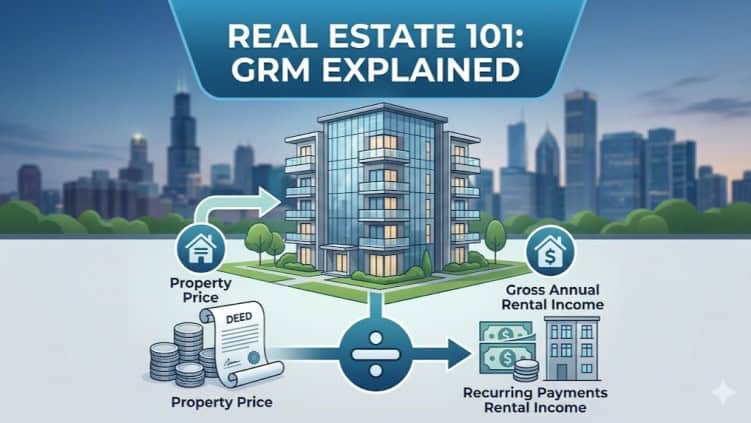

Math

Price divided by annual rent equals a number. That number is the Gross Rent Multiplier. A four-plex costs 800,000 dollars and brings back 160,000 dollars in gross annual rent. Divide 800,000 by 160,000 and you get 5.0. That means five years of gross rent equals the purchase price; take this with a grain of salt as it ignores every expense that determines whether you make money.

GRM is a screening tool, not an analysis. A lower GRM hints the price is reasonable relative to the rent. A higher GRM suggests you are paying a premium for the building, which means either the market supports it or you are overpaying.

The number itself is meaningless without context. A 5.0 GRM in San Francisco might be average. A 5.0 in rural Colorado might be terrible. You must compare similar properties in the same market to know what the number means.

Into Action

Investors use GRM a couple of ways. First, to compare competing properties quickly. Second, to estimate value by taking a known market GRM and multiplying it by the gross rent of a subject property.

If the typical GRM in your target neighborhood is 6.0 and the duplex you are looking at collects 120,000 dollars in annual rent, the rough value is 720,000 dollars. That is not an appraisal. It is an informed guess that keeps you from wasting time on properties priced far outside the market.

Pay Attention to Me

Here is where GRM, if you use it alone, can make you (as an agent or a newbie investor) understand that if you are not humble you will be humiliated; I’ve done it for you already. It ignores every expense that separates a profitable building from a money pit. Operating expenses, capital expenditures, taxes, insurance, vacancy, property management, and the cost of the tenant who stops paying rent in February.

Two properties can have the exact same GRM and produce wildly different net incomes because one has an old roof, inefficient utilities, or above-market property taxes. The GRM will not catch that. Cap rate will. Cash flow analysis will.

That is the limitation GRM cheerleaders sometimes forget to mention. Gross rent is the top line. Net income is what pays the mortgage. GRM looks at the top line and pretends the bottom line will take care of itself. It will not. You’ve still got to run the numbers, but GRM gets you out of the gate faster.

Agents

For agents working with investors, GRM is useful in two specific situations. First, when a client wants to scan a market quickly to identify which listings are even worth touring. Run the GRM on every comparable listing in the area. Sort low to high. Tour the low ones first.

Second, when a client wants to sanity-check a seller's asking price against what the building produces in rent. If the GRM on the listing is significantly higher than the neighborhood average, something needs to justify that premium, location, condition, potential, or maybe just a seller who has not looked at the actual rent roll.

The formula works in reverse too. If you know the typical GRM in a market, you can estimate what a property should be worth. Multiply the market GRM by the property's gross annual rent. The result is a rough value that keeps you from overpaying before you ever call the listing agent; check out this handy calculator.

Remember

GRM is not a replacement for underwriting. It is the first pass. It answers the question "is this worth my time" not "should I buy this." The folks who understand the distinction save their clients hours of busy work and position themselves as the person who knows how to filter a market efficiently.

When a client asks if a rental property is priced right, start with GRM. When they ask whether they should buy it, move to cap rate, NOI, and cash flow. One gets you to the door. The other tells you whether to walk through it.

This and a lot of my published work can be found on my website: americasells.com